Owning a property is a benediction. Property is not only beneficial in terms of economic, financial, business, agricultural or residential purposes; rather, the property may signify the emotional and religious feeling in nature of the Gift to someone or for religious purposes.

When we first look upon the term “gift of property”, we generally analyze that it is the Gift of any land. But here comes the turn, as such a Gift of property can either be of movable property or immovable property. Hence, in the eyes of the law, any person can gift anything from a pen, a toy to the glory of giving a house, car etc. Do you want to feel that sense of the recognition of gifting? So let us discuss the legal framework revolving around it.

Summary

- A gift deed is a vital document that needs to be drafted carefully.

- Well drafted gift deed is one of the convenient methods for transfer of property.

- All the mandatory requirements of creating a Valid Gift deed need to be fulfilled.

The first important question that comes to our mind is what does the Gift mean in legal terms? Or how can we say that particular act is an act of gifting? Or does any law define the term ‘gift’? So, section 122 of the Transfer of Property Act, 1882 in India describes ‘gift’. Generally, it is the transfer or conveyance of specific defined property, movable or immovable, by one or more persons, called donor, to one or more called the donee. Transfer of Gift will be considered fulfilled if that transfer is voluntarily and without consideration, whether monetary or not but does not include emotional consideration. On the part of the donee, the Gift will come in force only when donee or any person on his behalf accepts it. After the transfer by a donor, acceptance of the Gift by donee decides whether the Gift is made or not.

After getting the brief of Gift’s meaning, a lot of questions come to our mind, such as how can the transfer be made? Or who can be donor or donee? What can be transferred? And so on. How about discussing them gradually?

Table of Contents

Gift Deed

As we know that, a gift is a form of transfer of property. So, the transfer of Gift is made by way of a gift deed. A gift deed is a document depicting the transfer of a gift and its essentials such as the name of donor and donee, properties of Gift, date, witnesses etc. Is it necessary to make a gift deed? We can answer this question differently for movable and immovable property. In movable property, it is not mandatory to make a gift deed. Still, in immovable property and the drafting of gift deed, its registration is also compulsory under the Indian Registration Act 1908 section 17. A gift deed in respect of immovable property will become valid only if it is registered. Section 123 of the Indian Registration Act, 1908 renders the unregistered gift deed as invalid.

Essential Elements of Gift Deed

There must be donor and donee Who Can Be A Donor

A person can be a donor if he fulfils these two conditions as per section 7 of the Transfer of Property Act, 1882:

Competency

As the transfer of property is a form of contract, any person competent to agree can be a donor. Thus, any firm, company, HUF or juristic person can be a donor. However, a minor, unsound person or person otherwise disqualified by law is not entitled to be a donor. Example of a person disqualified by law: As per the Halsbury’s Laws of England, persons in fiduciary positions, e.g., trustees, agents or partners, are not entitled to make gifts of the vested property in them on behalf of others unless they are authorized to do so.

Entitlement

A donor can only be the person who is entitled to the transferable property, or in a more specific word, he is the property owner. Nevertheless, the person authorized by the owner to transfer the property as a gift can be a donor.

Recommended reading: When is a Succession Certificate Required

Who Can Be A Donee

A donee can be any person, even the person not competent to contract. A donee can be any living person and not an imaginary or future person. Any juristic person such as firm, company, or institution is a competent donee. Moreover, a minor, insane person or child in the womb can be a donee subject to lawful acceptance by them or on their behalf. On behalf of a minor, when a guardian approves, the minor can either accept it or reject it on attaining majority. Gift cannot be donated to the general public or unascertainable person.

Universal Donee

Subject to the acceptance of donee, when the whole of the donor’s property is transferred, then donee becomes liable for all the debts and liabilities, in respect of gifted property, of the donor existing at the Gift time. Such donee is universal donee.

There must be a transfer of ownership from donor to a donee

Transfer of Gift will not be fulfilled by mere promise to transfer or by only transfer of possession. The legal transfer of Gift requires transfer of ownership from the donor to the donee. Therefore, for a valid transfer of ownership, the donor shall himself be the owner of the property to be gifted.

Property transferred must be specific and existing

As discussed earlier, a Gift can be concerning a movable or immovable property. However, the property shall be defined and specific. That is to say, the property of the Gift should be clearly stated, and there should not be any doubt as to the identity of the property. The property must be existing and not future property. One can wholly or partly transfer the property.

Recommended reading: Process of Partition Lawsuit

The transfer must be voluntary with free consent

A donor cannot be forced to make a gift to any person, nor can donee be forced to accept the Gift. There must be free consent on the part of the donor as well donee. The words fraud, force, undue influence, misrepresentation, coercion or mistake should not be a part of a gift transaction to retain it valid. General authority in the relationship between donor and donee will not decide the validity of a transaction; undue influence in the case of Gift should be separately determined.

Transfer of Gift must be without consideration

Whether monetary or not, other than natural love and affection, any type of consideration makes the transfer of gift void, even a small or nominal amount of money or any undervalued thing as consideration will change the nature of the transfer from Gift to sale or exchange. Consideration in the form of spiritual or moral benefit such as taking care of a donor throughout his life is not considered.

The donee must accept the transfer during the lifetime of the donor

As already stated, the donee must freely accept a gift. About when such acceptance can be made, it is hereafter discussed. Acceptance of a gift offered can be made at any time during the donor’s lifetime or for the time the donor is competent to transfer a gift as per section 122 of the Transfer of Property Act, 1882. Further, this section stated that if the acceptance as to Gift is made after the donor’s death, such Gift is void. Acceptance of Gift can either be made by donee himself or any person authorized on this behalf.

For example, like in a company, a manager can accept a gift on its behalf; in trust, the trustee can receive the Gift and much more. When a gift is made to a person not competent to contract, any guardian or person on his behalf can accept a gift, but the donee on attaining competency may either accept or reject the Gift.

When there are more than one donees, a gift as to the donee who did not accept it will become void and other donees who have accepted it will be entitled to gift under section 125 of the Transfer of Property Act, 1882. For example Gift of a car is made to person ‘A’, ‘B’ and ‘C’, where ‘A’ declined the gift but ‘B’ and ‘C’ accepted the Gift. Therefore, Gift as to A will be void, and as to ‘B’ and ‘C’ will be valid. That is to say, B and C will jointly own that gifted car, and A will not have any role to play as to its ownership.

Recommended reading: Property owner search

Onerous Gifts

Onerous gifts are the gifts that carry obligation along with them. Transfer of Property Act, 1882 Section 127 deals with an onerous gift. When more than one, Onerous gifts are transferred in a single transaction, the donee can either accept the whole transaction or reject it wholly. When such gifts are transferred in a separate and independent transaction, the donee may accept some transactions and reject others. Acceptance of onerous Gift by a person incompetent to contract does not bound him until after becoming competent to contract and knowing of the obligations attached to an onerous gift; he retains the property.

Gift Under Hindu Law

Gift under Hindu Law may differ from general laws on these aspects.

Properties that can be transferred by way of Gift

Hindu Law specifies the properties that can be transferred by way of Gift, which are:

- Self-acquired property under Mitakshara School of law.

- Joint or self-acquired property under Dayabhaga School of law.

- Sole surviving coparcener can gift any or all ancestral property.

- Impartible property, unless prohibited by custom or tenure of alienation.

- A small portion of the property if a widow or father inherits that portion.

- Acceptance

Three ways of acceptance of gift.

Hindu Law specifies three ways of acceptance:

- Acceptance in mind without verbal communication or any expression of such acceptance, such acceptance is a mental acceptance

- Acceptance by verbally saying is known as verbal acceptance

- When acceptance is not verbally communicated but expressed through action and expressions, it is corporeal acceptance.

Other than these extras, Gift under Hindu Law is generally governed similarly to the Transfer of Property Act, 1882.

Recommended reading: Best ways to prevent property disputes in India

Gift under Muslim Law

General rules of Gift

A gift under Muslim law is termed as Hiba. Other than the general rules of Gift, the difference in the law of Hiba is:

- A donor must be Muslim.

- Guardian of incompetent donee for acceptance can only be out of following persons

- Father

- Father’s executor

- Paternal Grand Father

- Paternal Grand Father executor

In the case of Muslim Law, Hiba is of two types based on consideration:

- In Muslim Law only, a gift can be for consideration known as Hiba-il-iwaz.

- Gift without consideration is known as Hiba-ba-Shart-ul-Nawaz.

Revocation of Gift Muslim Law

Regarding the revocation of Gift under Muslim law, Gift can be revoked before the delivery of possession. But the revocation of Gift by the donor after the delivery of possession is not sufficient under Muslim law. A decree of the competent court for revocation of Hiba is required in this case. The donee can use the gifted property until the decree of a competent court as to the revocation of Gift is passed.

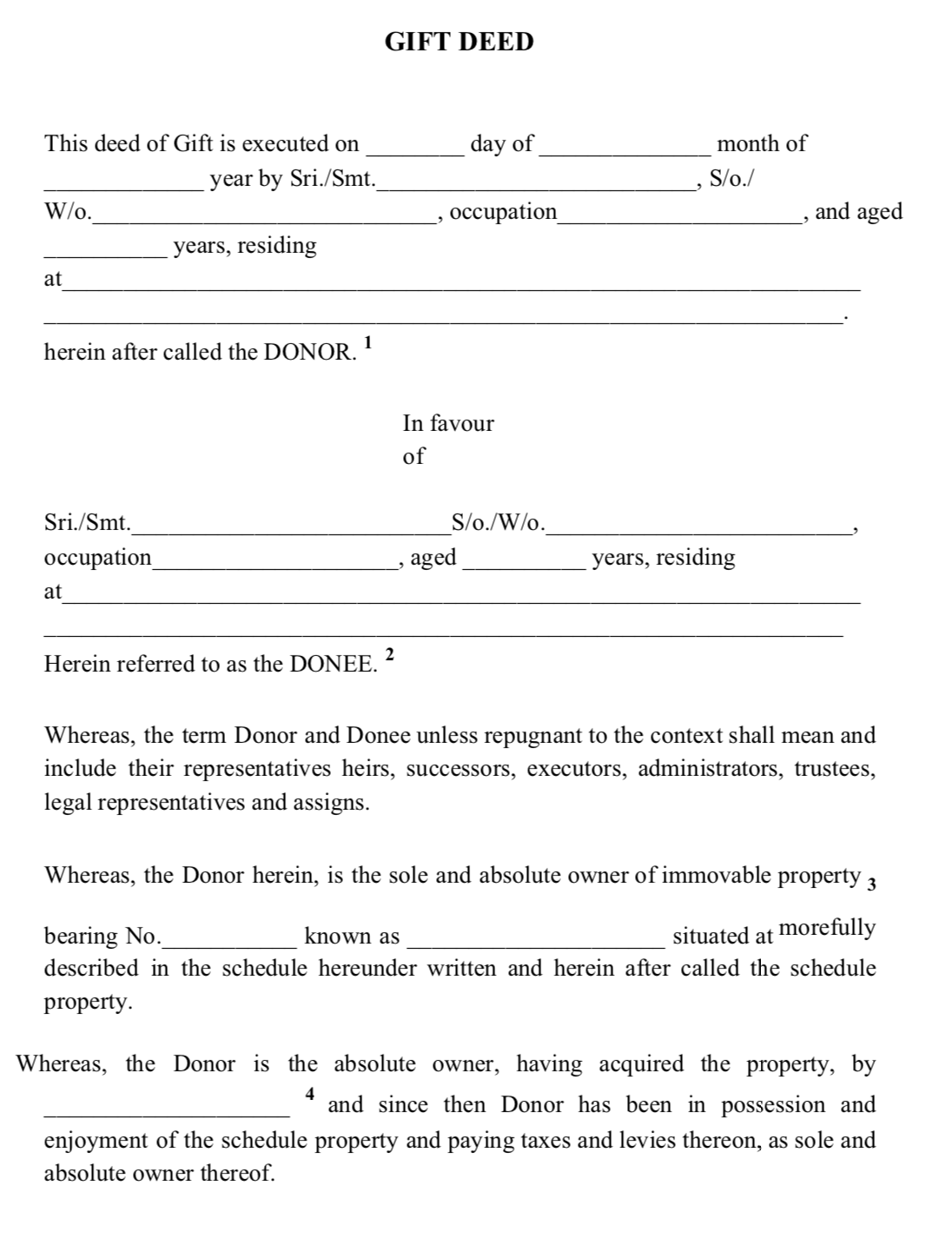

After studying the basics about the transaction of Gift, here are the clauses of the gift deed discussed.

Recommended reading: Landlord rights

How to Draft a Gift Deed or Steps in Drafting A Gift Deed

One can draft a gift deed on following steps:

- Firstly, a gift should be in printed form. Thereby, the details of a gift must be listed in the following manner:

- Give the heading’ Gift deed’ in capital letters.

- Then mention date of deed in legal language example: This deed is made on ___________ day of____________ month of ___________ year.

- The name of parties should be mention as “between

Donor & his details such as address, father’s name/Husband’s name, age, occupation etc.

AND

Donee & his details

- Then mention the term “WITNESSED AS FOLLOWS.”

- Then, in points, mention facts of transfer and important clauses of transfer.

- At last, a signature of donor and donee on each page, in the presence of witnesses and get the deed signed by witnesses.

- After documenting the deed, get it printed on applicable stamp paper.

{kind=link}

How To Register Gift Deed in India

The registration of gift deed of immovable property is compulsory irrespective of the value of a property.

For Gift deed registration, parties require specific documents, for say, PAN Card, ID Proof, any document proving the ownership title of the donor, depicting hid capacity to gift, Aadhaar Card. In addition, some States may require a valuation certificate of the property and an encumbrance certificate also.

The deed can be registered after the donor’s death, provided it is executed and accepted before the death.

Gift deed register steps:

- An approved evaluation expert will do valuation of a property.

- The gift deed will be documented.

- The gift deed will be signed by the donor or any person on his behalf and donee or any person on his behalf in the presence of at least two witnesses and get it attested, i.e., signed by witnesses.

- A signed gift deed will be submitted at the office of the sub-registrar nearest to the location of the gifted property.

- Lawyer services will be hired to calculate registration fee, stamp duty or other charges (Stamp duty and registration charges depends on male and female, agricultural or non-agricultural land, transfer in blood relation or non-blood relation, and varies from state to state) (Such costs depend on the value of the property) (latest charges are available on government official websites)

- Pay set out fees

After the completion of these requirements, the gift deed will be deemed as registered.

Recommended reading: Importance of Title Deed

Documents Required for Gift Deed Registration

You need to carry the following documents at the time of gift deed registration:

- Original Gift Deed

- ID Proofs, like Driver License, Passport, etc.

- PAN Card

- A document like a Sale deed to prove title ownership of the donor on the property

The list is open-ended; you might need other documents like certificates relating to the property’s value, depending on your state.

Know about the Stamp Duty in Each State at The Time of Executing a Gift Deed?

As per the Indian Stamp Act 1899, the stamp duty needs to pay by one, which varies from men to women and State to State. Besides the stamp duty expenses, property registration charges would also be applicable while gifting a property in India. Like stamp duty, property registration charges vary from State to State. Usually, property registration rates fall between 0.5 per cent-3 per cent across India, depending on the slab decided by the particular state.

List of stamp duty and registration charges as per the various states is discussed as under, which will help you understand the current stamp duty rates in the respective state.

| States | Stamp Duty Rates |

| Andhra Pradesh | 5% |

| Arunachal Pradesh | 6% |

| Assam | 8.25% |

| Bihar | Male to Female – 5.7% Female to Male – 6.3% Other cases – 6% |

| Chhattisgarh | 5% |

| Goa | Up to Rs 50 lakh – 3.5% Rs 50 – Rs 75 lakh – 4% Rs 75 – Rs 1 crore – 4.5% Over Rs 1 crore – 5% |

| Gujarat | 4.9% |

| Haryana | For male – 6% in rural areas and 8% in urban areas For female – 4% in rural areas and 6% in urban areas |

| Himachal Pradesh | 5% |

| Jammu and Kashmir | 5% |

| Jharkhand | 4% |

| Karnataka | 5% (above Rs 35 lakh)

3% (Rs 21-35 lakh) 2% (Less than Rs 20 lakh) |

| Kerala | 8% |

| Madhya Pradesh | 7.5% |

| Maharashtra | 5% for male

4% for female |

| Manipur | 7% |

| Meghalaya | 9.9% |

| Mizoram | 9% |

| Nagaland | 8.25% |

| Orissa | 5% for male

4% for female |

| Punjab | 7% for male

5% for female |

| Rajasthan | 5% for male

4% for female |

| Sikkim | 4% + 1% (in case of Sikkimese origin) 9% + 1% (for others) |

| Tamil Nadu | 7% |

| Telangana | 5% |

| Tripura | 5% |

| Uttar Pradesh | Male – 7% Female – 7%-Rs 10,000 |

Note: This is for information purposes only. These charges are applicable as on the year 2020-2021. Stamp duty rates may vary. One needs to refer to the Government website for the latest charges.

Recommended reading: Buying and selling property in times of Coronavirus

Tax Implication on Gift

The mode of transfer by Gift is subject to tax. Donor need not pay any tax on gift transaction. The donee has to pay tax as follows:

- In case donees receive a sum of money exceeding Rs. 50,000/- as a gift, through cash, cheque or draft, the whole amount is subject to tax during the previous year.

- Income from the Gift will be considered income from other sources under the Income Tax Act, 1961.

- Income from the Gift will be added to total revenue, and resulted in payment will be charged according to the tax slab.

- In the case of immovable property, if the stamp duty exceeds Rs 50,000/-, stamp duty will be chargeable to tax in such transaction.

- Amount of property received from the following relatives are tax exempted:

-

- Spouse

- Parents

- Brother or sister

- Brother or sister of the spouse

- Brother or sister of either parents

- Maternal or paternal grandparents

- Lineal ascendant or descendent

- Lineal ascendant or descendent of the spouse

- Spouse of any person referred to in c. to h.

- Gift received on the occasion of marriage and not only the day of marriage s exempted from tax.

- Gift of cash, whether in blood relation or not, above Rs. 2 Lakhs is subject to penalty.

Executing a Gift Deed vs Executing a Will?

Being two different ways to transfer Gift and Will, each has its advisability. However, a gift is preferable over will in these cases:

- Gift can be immediately executed, whereas Will can only be executed after the death of the testator.

- In case of transfer of property other than relatives, Law as to Will requires to take into consideration the interest of relatives, but that is not the case in the transfer of Gift.

- If you want to transfer a part of your estate, to avoid any litigation or other obligations around the properties, then, resorting to a gift is advisable.

Essential Clauses of Gift Deed

Draft of Gift deed shall consist of the following essentials:

- Details of the property gifted

- Details of donor and donee

- Clause of free consent of the donor

- Details as to the absence of consideration, and if the Gift is under Muslim law, specify the details of consideration

- Entitlement of donor to transfer the property

- Any condition for revocation

- In case of a minor, a person of unsound mind or juristic person, name and details of a guardian accepting a gift

- Clause of absolute transfer of ownership to a donee

- Any obligation of donee in reference to gifted property, if any, towards the donor

- Signature of donor and donee

- Name and signature of witnesses

Conditions When Gift can be Revoked

Revocation means suspension or cancellation of the contract of gift or gift deed. Now, we will see whether the gift deed can be suspended or revoked or not? If yes, how gift deed is revoked? Which provision of the law regulates such revocation and other related essentials.

Firstly, yes, a gift can be revoked. Such revocation of Gift is regulated by section 126 of the Transfer of Property Act, 1882. In accordance with this section, a gift may be revoked as follows:

- On an agreement between donor and donee to revoke the contract on the happening of a particular specific event. Revocation can take place only through such agreement and not through the sole Will/wish or donor. Gift revoked, wholly or partly, at the mere Will of the donor will be void.

- Gift can be revoked either wholly or partly.

- Gift can be revoked in any manner in which a contract can be rescinded other than on account of want or failure of consideration. For example: as per section 19 of the Indian Contract Act, 1872, a donor may rescind the contract if it is devoid of free consent. In case of the donor’s death, his legal heirs may revoke the contract on his behalf.

- Gift cannot be revoked on a ground other than mentioned above.

- The condition of happening of an event must be express and clearly stated. In the case of Mool Raj v. Jamma Devi [1], the High Court of Himachal Pradesh held that the condition of revocation of Gift, i.e., failure of the donee to maintain donor in future, was not mentioned in the gift deed. Therefore, the Gift was unconditional.

- In the case of Thakur Raghunathjee Maharaj v. Ramesh Chandra [2], the court held that it is not mandatory to stipulate the condition in gift deed; however, the condition may be defined in separate mutual agreement forming part of the transaction.

- Condition for revocation must be agreed upon at the same time as making the Gift. A gift once made becomes absolute cannot be revoked by future agreement. Therefore, while accepting the Gift, the donee shall also accept the condition for revocation.

- The condition for revocation must be a subsequent condition, i.e., it must be related to future events and should not relate to past events.

- As per section 10 of the Transfer of Property Act, 1882, the condition completely prohibiting property alienation, possession or ownership or right, avoids condition.

- If the condition for revocation is void, the Gift becomes absolute.

- If the Gift is further transferred to any person for consideration and that person is unknown of condition for revocation. The revocation will become void. For example, a gifted gold jewellery to B on the condition that D will teach A’s son until his son’s college life. B sold the jewellery to C, and C was not aware of the condition for revocation. D stopped teaching A’s son after the sale and before starting a college of A’s son. The Gift from C is not revocable as he is transferee for consideration and unknown of revocation condition.

Pros –

- A gift made to relatives is free of tax.

- A gift made to any person up to an amount of Rs. Fifty thousand will not attract any tax for both donor and donee.

- Registered Gift deed act as legally acceptable evidence to gift transaction, which makes it less prone to litigation.

- A gift deed is a quick way of transfer of property without complicated legal requirements.

- A gift deed can be revoked on the ground of forced transfer even after the Gift was completed.

Cons –

- A gift deed is compulsory to be registered in case of immovable property.

- There is a mandatory requirement for the presence of two witnesses.

- A gift deed may take away the inheritance right of legal heirs.

- A gift deed is irrevocable on a specified condition if that condition is made after the execution of the gift deed.

- Gift deed requires extra cost for stamp duty which varies from state to state.

Recommended reading: Repatriation of funds from NRE/NRO Account

Conclusion

This article outlines the essentials of the transaction of Gift, the content of the gift deed and tax applicable to gif transactions. As learnt, a gift deed is the documentation of the transaction of a gift. The Gift of both movable and immovable property is governed by the Transfer of Property Act, 1882. In general, as regard Hindus and Muslim, a gift is governed by their laws. Gift under Hindu law is similar to that under the Transfer of Property Act, 1882, but there exists a certain difference in Muslim laws.

It is to be remembered that tax exemptions are provided for our benefits, and we pay tax for our mutual benefit only. Therefore, a gift deed must not be used as a tool for tax evasion or any other illegal purpose. It is advised to take legal help from a civil lawyer to get the gift deed drafted as the deed’s language is vital to ascertain whether the document is a gift deed or any other transfer document. In any civil lawsuit, where the court has to find out the nature of the transaction, the words used in the deed describe the nature of the deed.

A gift deed is a vital document that needs to be drafted carefully. All mandatory requirements of creating a Gift deed need to be fulfilled to do a valid deed.

FAQs Gift Deed

A valid Gift Deed entails the followings conditions: –

- Gift must be accepted during the lifetime of the donor.

- Gift must be for the existing property; Gift in regard to future property is void.

- Gift to two or more donees that one does not accept shall become void.

- Gift has to be accepted with burdens or obligations imposed if any.

- If the Gift consisting of the donor’s whole property, the donee is personally liable to pay all debts due by the donor at the time of acceptance.

An NRI (Non-Resident Indians) or a PIO (Person of Indian Origin) is eligible to receive property as a gift. The donor has to be a resident of India/NRI/PIO. The property to be transferred as a gift must be either a commercial property or a residential property, but not agricultural land, plantation property or farmhouse in India.

As mentioned by you, the flat is still under construction. Therefore, execution of a gift deed in your daughter’s name will not be possible. Execution of the gift deed will only be possible when the property gets registered in your name. The Gift is possible on an existing property and not a future one.

A gift deed is a legal document that represents a transfer of a gift from one person to another. It is a valid document obtained after registering the transfer of a property to the beneficiary (donee). It is valid only if it is given out of love and affection, without any consideration.

The Gift Deed is similar to the Sale Deed. However, in a Gift Deed, there is no exchange of money. Registration Act, 1908 ( Section 17) and as per section 123 of the Transfer of Property Act, the property has to be be registered with the sub-registrar.

A person with a sound mind can be a donor and who is competent to enter into any agreement. Minors cannot be a donor.

A minor is not considered capable of entering into a contract. Any person who receives the Gift or transfer made to him is a donee. A minor can be a donee; nonetheless, the Gift would have to be accepted by the guardian of the minor donee on behalf of him or her.

No, cancellation and revocation of a registered gift deed cannot be done. On the other hand, one can seek legal remedy if the act was executed by coercion or undue influence on either party. However, an unregistered gift deed can be revoked as it holds no validity.

The income tax law states, that the gifts received by a person during a financial year is fully exempt, provided the value does not exceed Rs 50,000 in a year. If the value exceeds Rs 50,000 in a year, then the Gift will be taxable as income from other sources.

If the donee is a minor then in such a case, a guardian can accept the Gift on his/her behalf. The guardian serves as the manager of the gifted property. Once the donee is an adult, he or she can either accept or return the Gift.

Once the property is registered in the recipient’s name (donee), he is responsible for paying the remaining dues. To exemplify, a father executed a Gift Deed in respect of a house favouring his son, and his father had to pay Rs 20,000 as utility bills. Now, the son will be liable to clear the remaining dues.